Yields impacts on housing supply

Between 2017 and the end of 2021 the best or ‘prime’ yields for Dublin new build apartment developments, known as forward sale multi-family investments, were 3.75 per cent, writes Donald MacDonald.

This was what was consistently being secured by developers of these blocks, with funders able to underwrite investments at these levels. During this period, interest rates across the EU were at historic lows, with the European Central Bank rates at 0 per cent.

This allowed the investors to pay the low yields, and the pre-sale contracts allowed developers to secure workable finance terms for development funding which facilitated the construction of over 22,000 homes across the wider Dublin area providing accommodation for approximately 55,000 people.

It is worth pointing out that this new rental supply was only being seen in and around Dublin and not elsewhere in the country, despite there being dire need in other locations.

It was the increased interest rates from early 2022 onwards that had the most devastating results on new supply in the private rental sector (PRS). These increases, along with the Irish Government’s introduction of the 2 per cent rent cap in November 2021 and general sentiment towards real estate, decimated new rental supply commencements in Dublin.

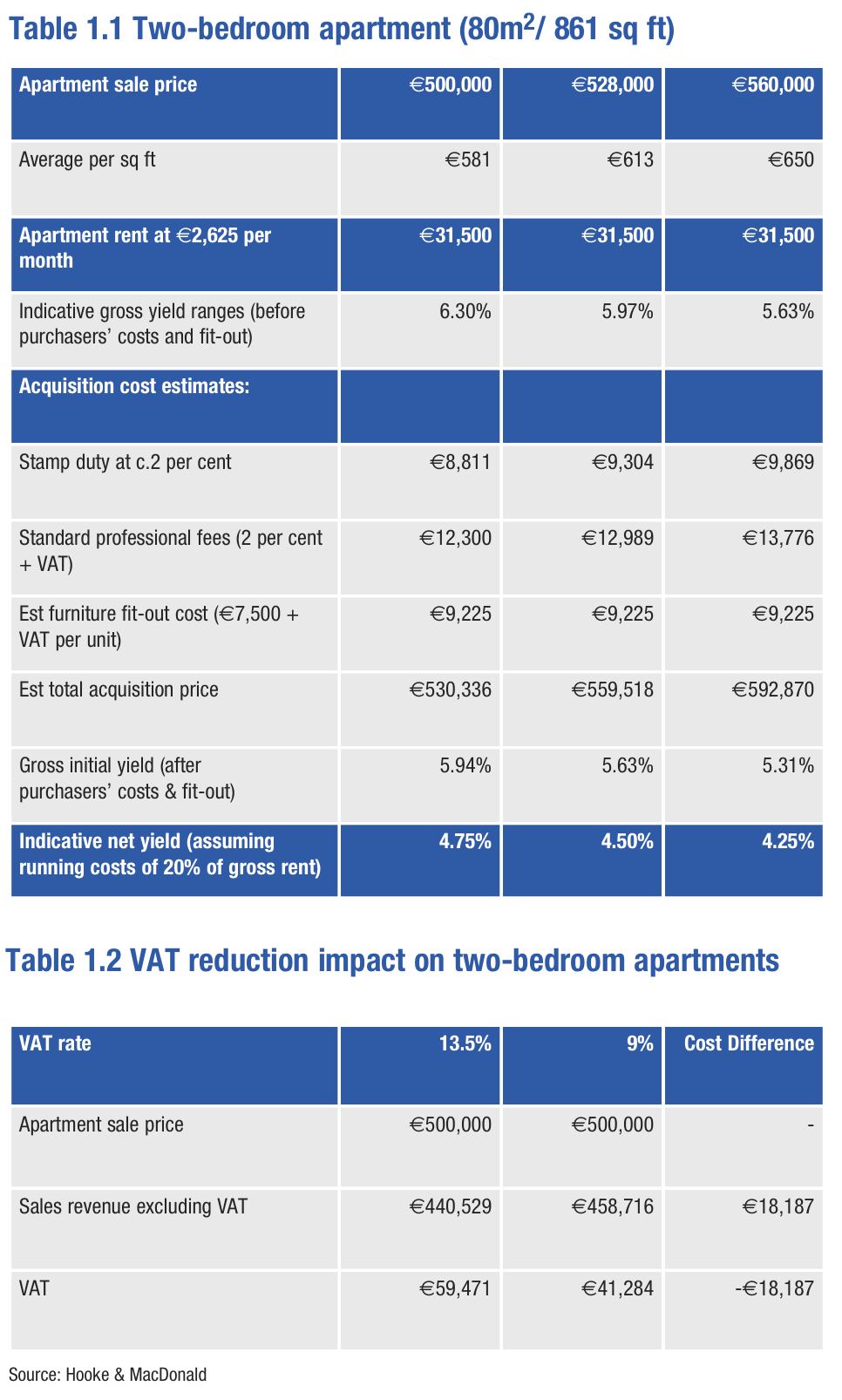

Today, the multi-family ‘prime’ yield is c.4.75 per cent in Dublin. A straightforward calculation for a two-bedroom apartment (see table 1.1 on the next page) shows where rents would need to be at for a developer of a new apartment today to sell it at €500,0000 to allow an investor to secure this return.

Table 1.1 also shows the increase in the apartment sale price at the same rent if the yield is compressed downwards; a very material difference of €28,000 for a 25-basis point decrease from 4.75 per cent to 4.5 per cent.

Apartment viability and VAT

In Budget 2026, the Irish Government reduced VAT to 9 per cent on new apartments. Then-Minister for Finance Paschal Donohoe stated at the time: “This reduction will help address the viability gap in apartment construction as part of a social policy to deliver more and higher density apartments.”

Table 1.2 on the next page illustrates the monetary consequences of this reduction on a two bedroom apartment.

The Society of Chartered Surveyors Ireland December 2025 report, The Real Costs of New Apartment Delivery 2025, puts the cost excluding VAT of delivering a new build two-bedroom apartment in a medium-rise suburban three- to six-storey block (category two) at approximately €500,000.

Capital need and yield trends

It is estimated by the Department of Finance that Ireland needs over €20 billion a year in funding to allow for the construction of 50,000 new homes, of which over €8 billion will have to come from private funders.

As with foreign direct investment, Dublin competes with other cities around Europe for capital. Residential investment net yields across comparable European cities currently range from around 3.75 per cent to 4.5 per cent, a good bit below Dublin.

Dublin net yields

At a macro level, Dublin has many positive factors that influence net yields for Irish PRS accommodation. For example, continuing and forecast population increases, as well as strong renter demographic need; housing supply shortfalls; Ireland is the only English-speaking member of the EU; and strong FDI; positive economic outlook and indicators, including Exchequer balances, strong employment, and good incomes in many sectors. All of these attributes also drive demand for rental accommodation.

At a micro level the quality of the new accommodation developed over the last 10 years by Irish developers is of an excellent standard, in many cases better than that being produced on the continent. This is recognised by investors.

One perspective is that if yields remain high in Ireland, this allows investors to get a better return. However, considering the viability challenges outlined above, if yields are high, then there will be more limited opportunities for new development of rental accommodation and investments that were made over the last 10 years are also challenged on capital value side, limiting liquidity.

What next?

2025 was remarkable in that there was appetite from multiple new and existing investors for residential multi-family investments in Dublin. About €400 million worth of transactions was conducted and there is currently over €350 million of stabilised portfolios at the latter stages of negotiations for sale.

The changes in rent regulations has been critical to this interest and have been welcomed in many quarters, but not by small investors.

As more liquidity comes to the sector, the market develops further and matures, there will be the opportunity for yield compression to bring Dublin net yields closer to other comparable European cities. This will assist increased delivery subject, of course, to prevailing interest rates and other external factors.

Hooke & MacDonald,

118 Lower Baggot Street,

Dublin 2

T: 01 661 0100

Donald MacDonald

E: donaldm@hmd.ie

W: www.hookemacdonald.ie