Budget 2023: Education

Budget 2023 delivered a record total budget of €9.623 billion for the Department of Education, with highlights including the State funding schoolbooks for all primary students for the first time, a reduction in third-level student fees and €860 million for capital spending that will cover 450 construction projects.

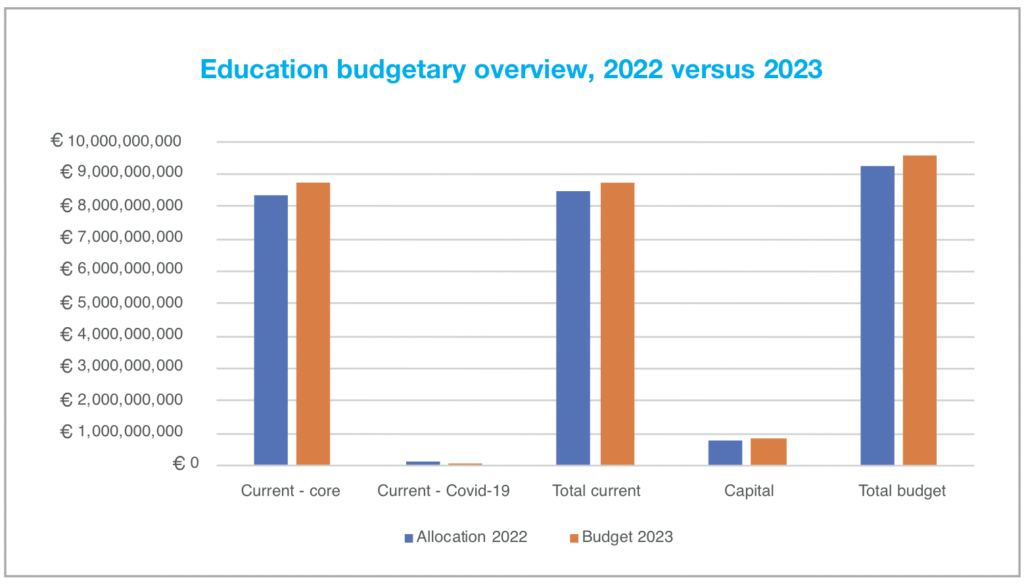

In total, Budget 2023 showed an increase of €351 million from the 2022 allocation for the Department of Education, a 3.78 per cent increase from the €9.274 billion provided in 2022. Core spending rose from €8,344 billion to €8.720 billion, a 4.55 per cent increase, Capital spending rose from €792 million to €860 million, an increase of 8.59 per cent. The only area of the education budget to experience a decrease, not unexpectedly, was Covid-19 specific spending, which fell from €138 million to €45 million, a decrease of 67.39 per cent.

Primary education

The increased funding will be felt especially in primary schools, where the landmark move to provide free schoolbooks for all of the circa 540,000 primary students in the State will see Ireland catch up with many other education systems, including that of the North. The move is projected to cost the State €110 per child and €47 million annually.

Primary schools will also see a reduction in class sizes due to the provision of an extra 370 primary teachers as a result of increased funding; from September 2023, pupil to teacher ratios will be reduced from 24:1 to 23:1. This measure, it is noted, is not the same as outright class size, but it is said that it will reduce class sizes. However, the State will still remain above the EU average class size of 20 despite this decrease in ratio; to achieve the average, it is projected that a ratio of 21:1 would need to be reached.

Special education

Budget 2023 has delivered a €13 million, or 85 per cent, funding increase for the national Council for Special Education, with the aim to “completely transform” the organisation. An additional 1,194 special needs assistants will be delivered via the budget, bringing the total to 20,368. 686 special education teachers will also be delivered through funding increases.

Third-level education

Third-level students will benefit from a one-time cost-of-living measure that reduces the €3,000 student contribution to third-level fees by €1,000; long-term plans relating to fees will see families with incomes between €62,000 and €100,000 have their fees decreased by €500 permanently, households earning between €55,240 and €62,000 will have their fees capped at €1,500, and households earning more than €100,000 will see their fees revert to €3,000. These cuts will be the first cuts in the student contribution in 27 years.

Grant recipients received a one-off double monthly payment, ranging from €56.11 to €679.44 depending on the category, and all PhD students on SFI and IRC awards will get a one-off €500 cost-of-living payment before Christmas. Long-term grant reforms will see student grants increase by between 10 and 14 per cent from depending on family income from January 2023. The most common grant of €3,025 would thus rise to €3,225 in 2022/23 and €3,677 in 2023/24.

School building

The €860 million capital spending budget will go towards supporting 450 construction projects, 300 of which are currently in the construction stage, and another 150 that are said to be at either the advanced design or tender stage. The construction programme is set to have an especial focus on the deliverance of additional capacity for special classes, particularly in special schools and at post-primary level.

Teachers’ unions’ response

Speaking after the unveiling of the budget, Irish National Teachers’ Organisation general secretary John Boyle, representing primary teachers, said that it “tackles the immediate over the important – while schools and families require immediate financial support, we must ensure Government keeps their promise to support primary school children in the aftermath of the pandemic. In that regard reducing primary class sizes to the EU average of 20 pupils remains key.” Boyle also welcomed the increase in school funding provision but stated that the budget “does not appear to address the chronic underfunding of primary education through permanent changes to the capitation grant”.

|

€9.6 billion total budget for the Department of Education 540,000 primary pupils to receive free school books 986 additional teachers in 2023 370 additional primary teachers 20,368 special needs assistants in 2023, an increase of 1,194 450 school building projects €100 million in one-off funding for increased running costs €1,000 reduction in the student contribution to third-level fees |

The Association of Secondary Teachers in Ireland (ASTI) said that the budget failed second-level education and would “do little to address the chronic underfunding of second-level schools and large class sizes”. “Ireland is ranked in last place out of 36 OECD countries for investment in second-level education as a percentage of GDP,” ASTI President Miriam Duggan said. “Despite this underfunding, Budget 2023 fails to address core funding for schools and does nothing to reduce our large class sizes. The funding gap experienced by second-level schools is not new and arose long before current inflationary increases. It is due to prolonged underfunding, and it is the reason why so many second-level schools are forced to fundraise to try to meet day to day operational costs.

“Schools continue to welcome more students every year, including students from Ukraine and other challenging situations. Teachers are addressing increasingly complex societal issues which are impacting on young people on a daily basis. Classes with 26 to 30 adolescents are the norm at Junior Cycle. Schools are buckling under the strain of increased demands and expectations.”